The digital nomad FIRE calculator you have been looking for does not exist in most of the tools you use daily. Revolut knows your spending. Wise knows your transfers. N26 knows your EU salary. Bunq knows your pots. None of them know when you will be financially independent. That is the gap we are filling.

You are not a tourist. You are not on a two-week escape from a desk in London or Austin. You are running a location-independent life, with three to five countries a year, income in a strong currency, and spending in whichever currency makes the month cheaper. The financial tools you already use understand that part of your life. The planning tools, for the most part, still assume you will die in the country you were born in.

This post maps the real nomad financial stack as it stands in 2026, names what every layer does well, and shows where the digital nomad FIRE calculator sits: the piece that turns a wallet full of banking apps into a timeline to independence.

Why Standard FIRE Calculators Fail Location-Independent People

The dominant FIRE calculators on the first page of Google were built for Americans who stay put. Most of them were good tools for that job. None of them scale to a life that crosses a border every quarter.

The defaults are specific. They price a US dollar. They assume a 22% effective federal-plus-state tax drag based on IRS brackets. They model cost of living against a single US city the user types in. They apply the 4% rule to US equity returns and US inflation. The entire architecture rests on one residency, one tax code, one currency, one zip code for life.

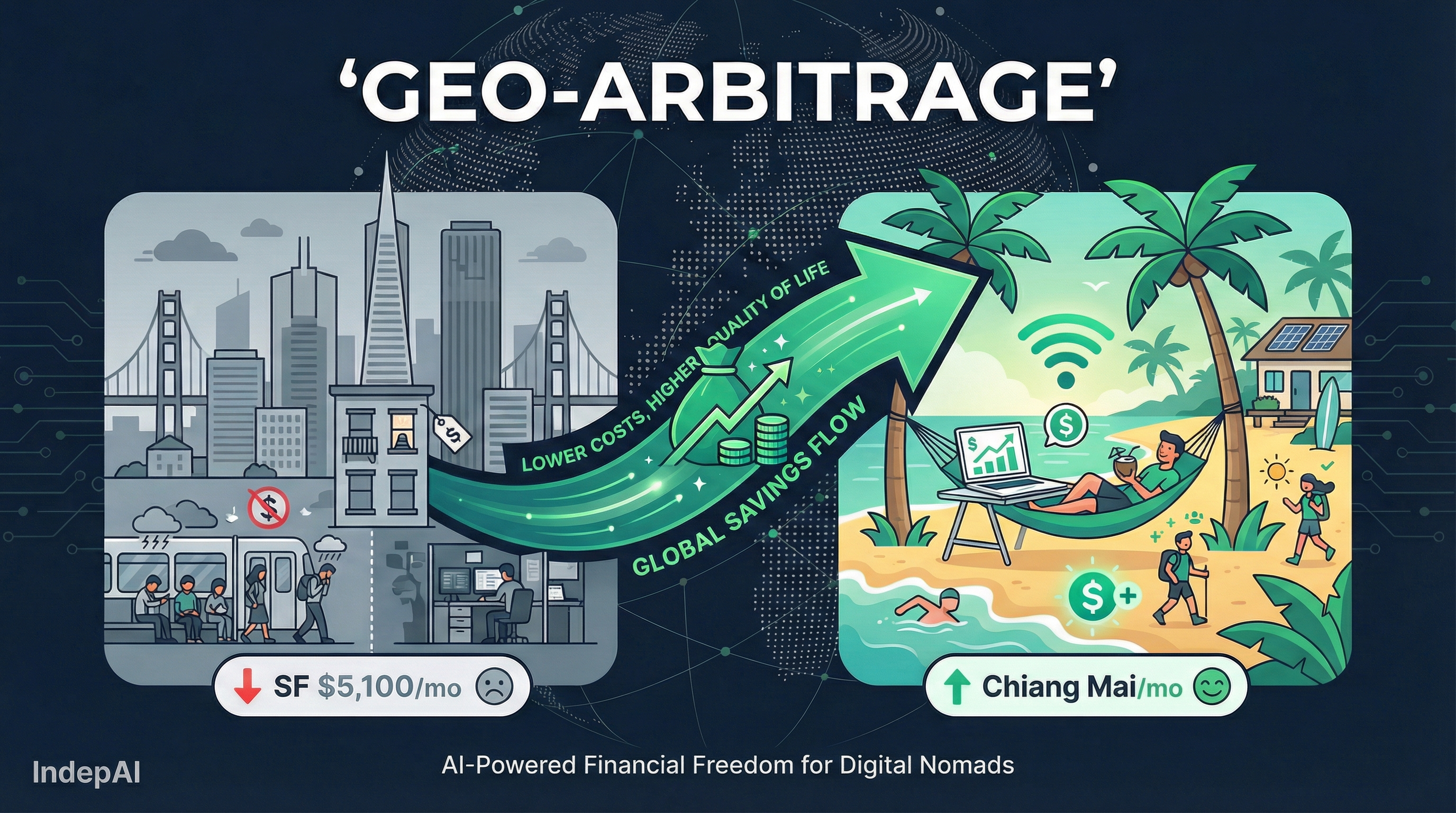

You violate all four assumptions before breakfast. A nomad earning $8,000 per month from a US LLC while tax-resident in Portugal under a Non-Habitual Resident regime, spending half the year in Bali and half in Lisbon, generates a FIRE number that depends on six variables the calculator does not expose. Currency: EUR, USD, THB, IDR. Tax: Portugal NHR, US self-employment, possible Indonesian 60-day rule. Cost of living: a $3,200 Lisbon month and a $1,600 Canggu month average to $2,400, not the $3,200 the calculator used. Investments: Portugal treats foreign-source dividends differently than the US does. Output: a FIRE number roughly 35% lower than the default tool reports, with a FIRE date pulled forward by five to eight years.

Miss that number and you either quit too early or grind too long. Both are expensive.

A digital nomad FIRE calculator has to take country, currency, tax regime, and cost-of-living path as first-class inputs, not as afterthoughts hidden behind “advanced settings”. That is the design constraint we built IndepAI around.

The Nomad Financial Stack in 2026

Talk to ten nomads on r/digitalnomad and r/ExpatFIRE and you will hear the same four apps on rotation, plus a fifth that is not a bank but lives in the stack anyway. Here is the honest map.

Revolut is the default card in almost every nomad’s wallet, the daily-spending and multi-currency layer. It holds 30+ currencies and spends at the interbank rate on weekdays up to a monthly allowance, with no foreign-exchange fee in most countries. It will not replace a local IBAN for long-term residency, and the premium tiers get expensive for features you rarely touch.

Wise is the lowest-friction way to move money between currencies. Earn in USD, owe EUR rent, and a Wise transfer usually costs a fraction of a wire. Its receive accounts in USD, EUR, GBP, AUD, and a few others let freelancers invoice clients in the client’s own currency, which quietly removes an objection you did not know was costing you work.

N26 is the EU residency-grade current account. If you are a non-EU national getting a long-term visa in Germany, Spain, Portugal, or France, N26 is often the first account that accepts you without a utility bill. Its German IBAN handles the SEPA direct debits for rent, gyms, and phone contracts that Revolut occasionally gets rejected from.

Bunq is the pots layer. It lets you carve one account into 25 sub-accounts, each with its own IBAN, which nomads use for bucket budgeting: one sub-account for next year’s Thailand visa, one for the next Mac, one for the brokerage top-up. It looks more like a personal-finance planner than the others, but it stops short of being one.

Nomad List is the odd one out, not a bank but a subscription data service: internet speeds, weather, safety, visa rules, and cost estimates across thousands of cities. Nomads use it to decide where to go next. It does not know your portfolio, so it cannot tell you what any of those decisions does to your FIRE date.

Five tools. Four cover the money. One covers the cities. None covers the plan.

A few honorable mentions sit adjacent to the stack without being in it. Monese and bunq-adjacent challengers handle edge-case residencies. Interactive Brokers is where most nomads park the brokerage layer because it supports multi-currency funding and is tolerant of address changes across borders. Trade Republic is gaining ground in the EU for the same reason. Charles Schwab’s international brokerage keeps US-citizen nomads compliant. None of these are a FIRE planner either. They are where the portfolio lives, not where the plan lives.

Banking for Digital Nomads FIRE: What the Stack Is Actually Optimizing For

If you zoom out, the nomad banking stack optimizes three things at once. First, friction: making it easy to pay a Lisbon landlord in EUR while your income arrives in USD, without losing 3% to a mid-tier correspondent bank. Second, compliance: making sure your account accepts a Portuguese NIF, a German Meldebescheinigung, or a Thai work-permit address without freezing the moment you move. Third, visibility: one screen where you can see USD, EUR, PLN, and THB balances in the same glance.

The stack does not optimize for the fourth thing a FIRE pursuer actually needs, which is a time axis. Revolut does not plot a compound-growth curve. Wise does not model a withdrawal rate. N26 does not compare your after-tax income against a city-specific FIRE target. That is the layer we are building, and it is why “banking for digital nomads FIRE” is a slight misnomer. No bank is going to give you a FIRE date. A planner will.

What’s Missing: the Digital Nomad FIRE Calculator That Ties the Stack Together

Here is the workflow gap we keep hearing described on Reddit, in ProjectionLab’s feature-request board, and in the Mustachian Post forum: you have the money moving correctly, but you do not know what the money is doing to your finish line.

The gap has a specific shape. You can see your Revolut balance today. You can see what it bought you last month. You cannot see how a decision to relocate from Berlin to Porto in Q3 changes the year you retire. You cannot see what happens to your timeline if the euro weakens 8% against the dollar next year. You cannot see whether spending six months of the year in Malaysia instead of Portugal lets you pull your FIRE date forward by two years, or three, or none.

That is the digital nomad FIRE calculator the stack is missing. Not another budget app. Not another card. A planning layer that takes the multi-currency, multi-country, multi-tax reality the rest of the stack already handles and resolves it to one number and one date.

The calculator has to do three things your banking apps do not:

One, it has to hold your FIRE number as a function of location, not a constant. When you change country in the planner, the number changes. The IndepAI FI calculator treats the number as a range across countries from the first input, not a single line that shifts only if you dig into settings.

Two, it has to model the arbitrage, not just the snapshot. The IndepAI geo-arbitrage tool compares 11,400+ livable cities on cost of living, tax, and visa path at once, so you can see where the money goes furthest and where your FIRE date moves forward the most. We have written this framework in more depth in What is Geo-Arbitrage.

Three, it has to respect the fact that a nomad life is not linear. You will not spend the next 20 years in one city. You will spend three years here, two there, one testing a city that turns out to be a mistake. The planner has to accept a sequence, not a single location. A year in Porto, a year in Chiang Mai, a year back in Warsaw. The FIRE date rolls with the sequence.

How IndepAI Fits: Not a Bank, but the Planning Layer

We want to be clear about what IndepAI is and is not. We are not replacing Revolut. We are not asking you to move your euros off Wise. We are not opening current accounts. The four fintechs above are excellent at moving and holding your money. We sit above them.

IndepAI reads the shape of your stack, the currencies you hold, the countries you work from, your monthly burn across cities, your taxable residency, and returns three things the stack cannot produce on its own. A personal FI Score on a 0-to-1000 scale, updated live as you change assumptions. A ranked list of countries and cities where your current portfolio is already enough for financial independence and where it would be enough in 1, 3, 5, or 7 years. And a calendar-year view of the trade-offs: live in Porto this year and save 12 months off your FIRE date, live in Warsaw the year after and save another 10.

That is the planning layer. It does not hold your money. It tells you what your money means.

“I was looking at another 7 to 10 years of grinding in the US. Then I realized I could live my ideal life abroad for less than $2,000 a month. The math was undeniable: I was already there.” That is Jack Wilson, a former software engineer who FIREd to Ecuador, quoted in a 2024 Rewire Abroad profile. He figured the math out with a spreadsheet. Most people will not. That is our job.

What “Pioneer” FIRE Actually Looks Like: Three Vignettes

We want to put real numbers against the theory. Three common nomad profiles, three countries, three FIRE dates that do not resemble each other at all. All three use public 2026 cost-of-living data from Numbeo and the cities already covered in IndepAI’s dataset.

Portugal: Maria, 34, UX designer earning EUR 72K remote

Maria earns from a Berlin agency as a contractor. She moves to Porto on a D7 passive-income-friendly visa. Her rent drops from EUR 1,550 in Kreuzberg to EUR 950 in Cedofeita. Her grocery basket drops 35%. Her marginal tax rate under Portugal’s post-NHR regime lands around 20% for most of her design income in 2026. Her monthly comfortable cost runs EUR 2,600.

Her FIRE number at 4% moves from EUR 1.04M (Berlin monthly EUR 3,450) to EUR 780K (Porto). At her 40% post-tax savings rate, that pulls her FIRE date from roughly 14 years to 9.5 years. Same salary. Same job. Four and a half years back.

Bali: Tom, 38, solo SaaS founder at $15K MRR

Tom runs a B2B SaaS with $15K monthly recurring revenue, mostly US and UK customers. He holds an E33G (now referred to as the Bali Remote Worker KITAS) and splits his year between Canggu and Ubud. His monthly burn is $1,800 including $450 for a villa, $300 for motorbike plus fuel plus insurance, coworking, and the occasional flight out. His effective tax is complicated. He runs a US LLC taxed as a disregarded entity and tracks Indonesia’s 60-day stay-threshold rule carefully, which lands him near 18% blended.

His FIRE number at 4% is roughly $540K if he plans to spend the next decade on a Bali-Lisbon rotation. If he plans to move back to the US in ten years, the number is closer to $1.3M because the withdrawal will happen under US cost of living. Two different plans, two different finish lines, one person. Our calculator tells him the date for both and shows him what happens if he changes his mind.

Warsaw: Anna, 31, data engineer at a Berlin fintech

Anna grew up outside Poznan, studied in Berlin, works remote for a Berlin Series-B. She earns EUR 95K gross and Warsaw is where she wants to live. Her cost of living runs roughly EUR 1,700 monthly including a comfortable flat in Mokotow. Her Polish lump-sum tax regime for B2B contracting lands her effective rate near 12% on her service income.

Her FIRE number at 4% is EUR 510K, roughly half of what a peer doing the same job from Munich needs. Her projected FIRE date is 8 years. The Berlin version of Anna is 13. Same company, same title, same code, five years faster because her zip code is in Central Europe, not Western. We wrote about the math behind this in Best Countries for FIRE 2026.

Three people, three countries, three finish lines. A US-default calculator would hand each of them the same Ohio-shaped answer. Every one of them would be wrong.

Join the Waitlist

We are opening IndepAI to a first wave of early users through the waitlist. If your everyday stack is Revolut, Wise, N26, Bunq, and Nomad List, the calculator we are building is for you. The math is specific, the output is a date, and the inputs respect the life you actually live.

Drop your email on the IndepAI waitlist and we will bring you into the calculator early. You keep your banks. We handle the plan.

Built in Krakow. Scaled globally. For the generation that does not retire in one country.

Know your number. Know your city. Know your date.

They told you to save harder. Check the city lever.

Most FIRE calculators assume you never move. IndepAI shows how your FI date changes when your city changes.

Private build. No spam.